This is a very quick post, as today the news covered the ongoing delays to sorting out the Post Office scandal and another case is going to court.

–

Solution – What i would do if it was up 2 me

–

Pardon all those who have been convicted. We are wasting time and money at the moment, just do it. I never thought I would agree with the way Donald Trump deals with things but we need the equivalent of an executive order.

Set a level of compensation for:

those who have been convicted and sent to jail (proportional to sentence)

those who are convicted but not sent to jail

those who lose their jobs as a result of being accused

those who left their jobs due to being accused

In addition, recompense of the costs those who paid monies to the post office

Charge Horizon withe the costs and if required, sue for negligence

Highlight all those persons who pursued criminal cases when it was known there was flaws with the system. They should be considered to have perverted the course of justice.

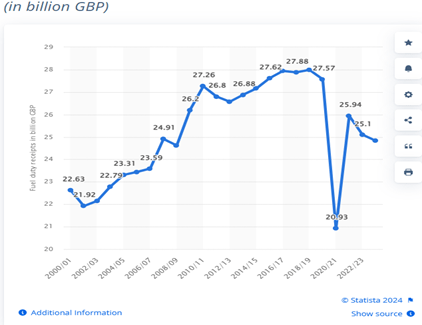

Over the past five years, the UK Government has witnessed a significant reduction in fuel duty revenue together with a decline in car BIK (Benefit in kind) revenue.

The loss over the last 5 years is circa 3 Bn per year for fuel duty alone.

–

This decline can be attributed to the increasing adoption of electric vehicles (EVs), which do not attract fuel duty. So the revenue from fuel duty is only going to decrease as more and more people shift to Electric Cars.

–

The Decline in Fuel Duty Revenue

Fuel duty has historically been a significant source of revenue for the UK government. However, in recent years, this revenue has been on a steady decline. Fuel duties, which once contributed as much as 8% to the annual tax revenues, have now dropped to around 4% over the last four fiscal years . it will decrease further over the coming years.

–

The Rise of Electric Vehicles

The adoption of electric vehicles in the UK has been growing rapidly. In 2023, the number of electric cars registered in the UK reached 455,200, a 23% increase from the previous year . By the end of June 2025, there were over 1.55 million fully electric cars on UK roads .

–

Whilst the government has started to address the shortfall, I do not think it is sufficient to fill the gap and is therefore adding more pressures on other taxes and government expenditure.

–

Cost Comparison: Public Charging vs. Home Charging

–

There are 3 factors that affect the adoption of Electric Vehicles

–

Firstly, no road funds licence. Whilst the government has introduced a modest fee, this is not in my mind sufficient to offset the loss in revenue.

–

The second factor that is influencing the adoption of electric vehicles is the cost of charging. Charging an electric vehicle at home is generally more cost-effective than using public charging stations. The average cost of electricity in the UK is around 34p per kWh, (I pay 25p per Kwh) making home charging significantly cheaper. In contrast, public charging stations can cost around 50p per kWh for fast charging and up to 73p per kWh for ultra-rapid charging .

–

These figure are interesting when you compare to the wholesale electricity currently cost of 8.69p per Kwh. (according to Energy Stats UK). Assuming 70p per Kwh, at the charging point, 20% VAT 12p less 9p wholesale cost, this gives 49p to the supplier. However, at home at a charge of 25p per Kwh (what I am currently paying for electricity) and VAT at 5% (1.25p per Kwh) the supplier gets 14.75p per Kwh.

–

My conclusion is that, the supplier for a service station charges are getting over triple that your domestic supplier is getting, which does not make sense to me. I believe that the charges at the service station charges are charging a rate compatible with Petrol and Diesel costs, even though they are heavily taxed. The charger providers are making the equivalent to the fuel duty on the petrol and diesel that would otherwise go to the government. They are doing this because they can and people will pay as there is not enough competition due to lack of charging points.

–

I accept that there is a capital expense in installing a charging station, but no more so than a petrol station, so why should they make significantly more money.

–

Thirdly, the benefit in kind (BIK) for electric company cars is ridiculously low. Currently the BIK is now 3% which means someone with a £40,000 company car in the 20% tax bracket would only pay £20 per month. That is one hell of a benefit and does not reflect the actual benefit. To lease an equivalent car would be over £300 per month. So it is no wonder 50% of company cars are now electric.

–

So What would I do

Have all cars subject to a minimum road tax of £195 as current level.

I would have a sliding scale for cars based upon their power. It is the way they tax ICE (Internal Combustion Engines) cars so this should be applied to Electric Vehicles. In essence a car that can accelerate from 0-60 in under 4 seconds will use more electricity than a car that achieved it in 8 seconds. You can even buy a small Volvo SUV that can accelerate from 0-60 in 3.6 seconds. This is ridiculous. The sliding scale I would implement would be £100 per second under 8 seconds. Given the average mainstream EV acceleration is under 6 seconds, this would generate £2.2 bn to £3Bn

I would also adjust the BIK (benefit in Kind) for company electric cars. I would charge a BIK that is the equivalent tax of £100 for 20% tax payers and £200 for higher rate taxpayers. This would add at least ½ Bn to 1Bn in tax revenue.

I would add 20% charge for the equivalent of fuel duty. Whilst in theory, this would increase the cost by 20%, I believe by increased competition as more charging station appear, this cost will be absorbed into the overall cost. As I explained earlier, the current suppliers are making too much. I believe this would generate 0.25 Bn

I would have the equivalent of Ofgem, to monitor these costs and if necessary, implement a price cap. It works for our domestic supply so why not for Car charging.

The above would apply to all cars, EV or ICE and would rectify the decline in revenues from Fuel Duty etc due to electric Vehicle. However, I would make electric vehicles subject to 10% VAT and Hybrid subject to 15% VAT producing a £4000 saving on a New £40k EV. How would this be paid for? I expect this to pay for itself as it will encourage additional purchases of New EV’s, in significant higher numbers than before. I would go further and reduce UK made EV cars to 5% VAT to encourage investment in the UK. I have, whenever possible bought (8 out of the last 9 cars) British Made cars and anything that encourages home grown products has to be a good thing.

Conclusion

The reduction in fuel duty revenue, coupled with the rise of electric vehicles, presents a significant challenge for the UK government. While the transition to electric vehicles is essential for environmental sustainability, it also necessitates a re-evaluation of the tax system to ensure that government revenue remains stable.

Today was the third day in a row that we received 3 pieces of the same junk mail, and on 1 day, we received 2 copies of the same thing, Royal Mail, Ocardo and McCarthy Stone. So 4 copies of each in 3 days.

–

It crossed my mind that is a huge quantity of Junk paper that is being delivered and disposed of each day and I have to pay for with higher council taxes.

–

So just how much junk mail is being delivered?

–

There are 28.4 million households in the UK and if each have 20g (3 pieces) of Junk delivered for 4 days per week, that equates to 568 t per day (568,000kg) or 118,144 t per year. (studies have shown on average 650 pieces of junk mail are distributed to each household per year , giving a total of 17.5Billion per year)

–

This is therefore costing at least £15m per year to dispose of. Whilst this is not much in the scheme of things, it is just a “waste of paper”.

–

For my local council, Chester and Cheshire West, we are disposing and estimated 480t per year in Junk Mail.

–

This is also not doing anything for the environment.

–

So what would i do.

–

I would ban junk mail distributed without a licence. If you do distribute, you will have to purchase a licence from your local council.

–

For small businesses with turnover less than £250,000 per year, the licence will cost £100 per year if delivered by hand by an employee of the business.

–

For larger businesses with a Turnover over £250,000, the licence is £1500 per council district plus 1p per piece.

–

The benefits of the above is that this will either discourage the ever growing trend of Junk Mail or providing an income to the councils who have to deal with the waste.

–

I hope this will actually reduce the waste, but if companies continue to target household without their consent, they will have to pay for the privilege.

I read an article today from the BBC news ” Trump delays tariffs as the rest of the world plays hardball” and noted the effect on trade from China.

–

In this report, it records Chinese exports to US has fallen by 9.7%. In 2024, the Chinese exported $525Bn worth of goods, so a reduction of 9.7% reduced the US import by $51Bn to $474Bn

–

However with the current tariff is now 30%, up by 11% from 2024. This means that an additional cost of of $52Bn. is added to the cost of imports.

–

Conclusion is that the US economy is getting less goods for the same price!!, i.e less product for more cost, which will only make the economy poorer. It is also likely to increase costs further, due to the most basic of economic theories, supply and demand.

–

Furthermore, China has increased its exports to the rest of the world by 6% (ref BBC) meaning an additional $205 Bn of exports. So the US tariffs is no more than an inconvenience.

–

Advertisements

So what would I do,

–

Well, we are where we are, and given the National Debt, I agree the need to increase taxes. As tariffs are just another tax, it is one of the many ways to increase tax (I consider the tariffs is only another form of sales tax, it is just applied at a different part of the supply chain) And to some extent, it will encourage some re-shoring,

–

I think a more structured implementation would have been more beneficial so as not to alienate your closest of friends. Trying to beat someone up never works in the long run.

–

I would have targeted those industries I want to protect in my own country or those industries i want to encourage to re-shore. I would not target specific countries.

–

In conjunction with this, I would also give tax breaks to those industries / companies that do re-shore or set up in my country.

Currently, the ISA allowance is £20,000 per year, that allows someone to save up £20k and the returns from these investments are Tax Free, be it stocks and shares or cash.

–

Approximately 1.8 million of the UK population use the full £20k allowance and most / i would say all are higher tax earners. The reason i say this is that i do not believe anyone earning under £50 per year could save £20k per year, i.e 50 % of their total take home pay.

–

This allowance therefore, disproportionately benefits the wealthy as most people do not have that level of disposable income to save £20k per year. The figures show that the majority of those with ISA’s save less that 5k per year, according to AJBell.

–

Advertisements

The result of this policy is that the rich get richer but only as a consequence of they having money, they do not earn this extra benefit.

So what I would do

–

I would reduce the allowance £10k. This would result in approximately 1.8 billion of investments being outside the ISA envelope per year generating £0.72 Bn of tax in the first year. For each subsequent years it would increase by 0.72 Bn so after 5 years, it would be producing £3.6 Bn of revenue. This does not include the added value associated with compounding and those on 45% tax.

–

This would only affect less than 5% of the population.

–

I am not for taxing the wealthy for the sake of it, but I think the tax system should be fair across the board. With this situation, I think the ISA rate disproportionately benefits the wealthy.

–

I would also limit the value able to be held in an ISA.

–

Did you know that:-

There are nearly 5,000 ISA millionaires in the UK, according to recent government data. This number has been steadily increasing, with a near 10-fold increase since 2016. The number of ISA millionaires has risen significantly in recent years, with a substantial increase from 450 in 2016 to nearly 5,000 today.

–

The average ISA millionaire has a portfolio worth around £1.4 million, according to Aberdeen Group plc.

Advertisements

–

The top 25 ISA investors hold an average of nearly £9 million each. This means that these individuals receive over £0.5million per year tax free!!

–

So what i would do here is limit the value of ISA initially to a maximum of £1m. Whilst this would increase revenue by a relative modest amount in terms of government taxation, £50m, it would be a fair way to raise taxes on unearned income.

–

I would also have an allowance of ISA that you can pass over to your children that is not subject to inheritance Tax. That will be dealt with separately when I cover inheritance tax, in particular with the inclusion of your pension pot inheritance tax calculations from 2027, which i think is totally unfair.

I consider the biggest hinderance to the housing market is the middle band of stamp duty between £250 and £925k.

Using myself as an example, I am lucky enough to have a nice 4 Bed house in a nice area in Cheshire. It is a good Neighbourhood with good schools, close motorways, train stations and airports. Ideal when you have a young family.

The approx. value of this house is £550 to £600k

Now, I have considered moving to a different part of the country, perhaps downsizing in terms of size but have a bigger garden, larger garage etc

However, if I looked at a £600k house, it would cost me £20,000

And if I chose to move further south closer to my grown-up family, where house prices are more expensive, the stamp duty increases significantly.

So, I and many of my generation, who moved to an area of good schools 20 years ago, have now become a blocker to younger families who want to live in the area and are unable to do so as there are not enough houses on the market.

The consequence are: –

that there are less children in the local schools residing in the local village. (I say village but with 7500 residents). More children must travel. The consequence of which are children do not walking to school (health benefits) and more traffic.

there is a shortage of houses in areas they are needed

there is less tax revenue as less people moving.

less stimulus in the housing market and associated trades

the tax man gets no money out of me as I do not move.

It can be seen from the statistics that the revenue on Stamp Duty has fallen from £11.7Bn in 2022/23 to £8.57Bn in 2023/24 and the number of house moves have fallen from 1.06 million to 0.872million over the same period. So we can see, the trend is down causing more of a shortage in the housing market.

So. what would I do if it was up 2 me, I have 2 ideas.

Option 1 – Changes to Stamp Duty Rates

Any House between £150k and £1million would be subject to a 2.0 % levy. If the market stayed the same as 2023/44, this would reduce the tax take by 2.5Bn.

However, I consider this will stimulate the market and increase the number of transactions. If this only increase to 2021 / 22 levels, there will be an increase the number of transactions by 39% in the under £1m price bracket.(yes that is the amount it has fallen in 2 years , number of transactions have fallen to 845,000 from 1,175,000)

So, on the basis of this will stimulate the housing market in third and fourth time buyers sector, and the levels only reach 2021/22 levels, the tax take would be £3.552Bn, a shortfall of £1.167 Bn.

In addition to the above, house prices have increased by 6% over the last 2 years so the revenue will increase by £0.2Bn for houses under £1m and by 0.23Bn for those over £1m

This gives a total receipt of £4.0 Bn

So, in theory, I am costing the country £ 0.7Bn. How am I going to pay for this.

The government has promised 1.5 million new homes over 5 years which equates to 300,000 per year which would cover the 0.7Bn shortfall.

So the above, in my opinion would be revenue neutral as it would stimulate the housing market sufficiently to offset the lowering of taxes.

Option 2 – Pay on the difference

This is the option I would prefer, and I think it is the fairest.

The basis is that you only pay a %age on the difference in house value, so that you only pay on the increase.

If you sell your house for £400k and buy for £550k, you pay on the difference of £150k. I do not have any data on the difference, so I have just made an assessment.

So based upon 1.2m transactions, that would generate at 5%, £9.3 Billion, more that recovered in 2023/24.

The additional benefits of stimulating the housing market will be felt across all the building trades, from plumbing, extensions, patios, conservatories DIY etc as more and more people will want to improve their new homes. This will create more jobs and greater tax revenue.

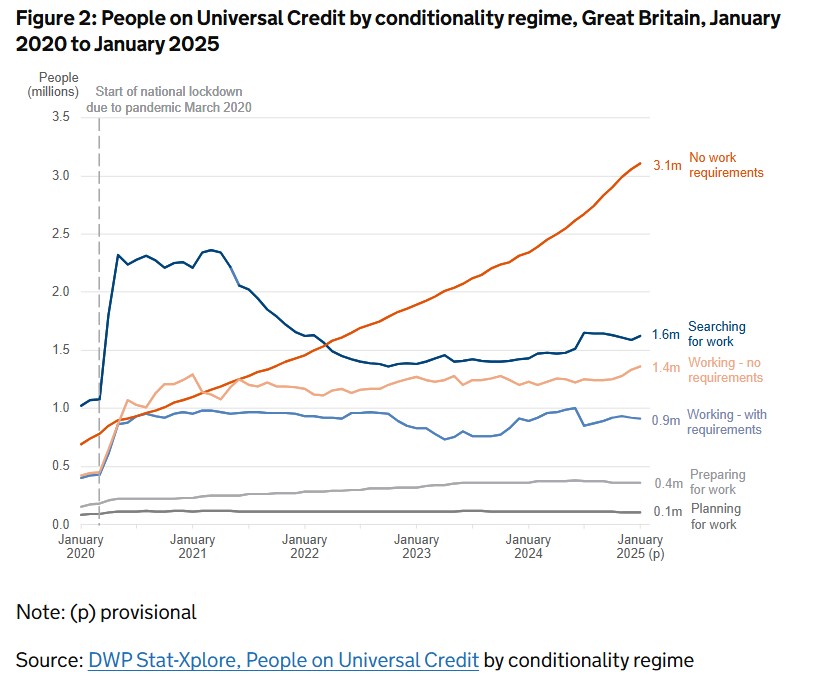

I came across this chart from the Government showing the massive increase in the Universal Credit Claimants with “NO WORK REQUIREMENTS”

Since 2000, those claiming Universal Credit with a “No Work Requirement” has increased by 400%.

That is almost 10% of the working population.

One of the many reason we spend £90 Billion (£90,000,000,000.00) per year on Universal Credit.

I do not believe we have 4x as many people are unable to work than in 2020.

If we could get 25% of these off Universal Credit, we would save £10Bn, enough the increase our policing by 50%, but 25% should not be the target, we should be looking reducing the No Work Requirement element back to 2020 levels, saving a massive £35,Bn.

A total overall of the Welfare and Universal Credit system is required, I do not claim that I understand how Universal Credit is meant to work, but if the country is to avoid going bankrupt, this has to change.

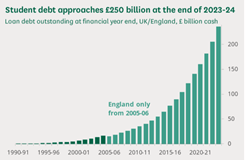

Analysis and Recommendations on UK Student Debt and Interest Payments

–

Challenges, Current Situation, and Potential Reforms

–

The issue of student debt in the UK has become both a financial and political challenge, with implications not only for graduates, but for the national balance sheet and future taxpayers as well. Recent figures and trends underscore the mounting scale of the problem.

–

The Scale of the Challenge

Adjusting for average inflation at 2.5% over recent years, the total cost of the student loan programme now exceeds £250 billion in today’s money.

–

–

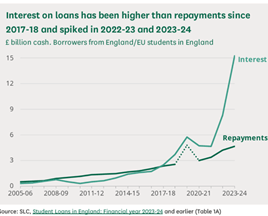

Higher interest rates, particularly those implemented from September 2022, have sharply increased the burden of student debt. Interest added to outstanding loans soared to £8.3 billion and £15.3 billion in 2023-24 alone. In the latest year, the interest capitalised on student debt was three times the value of repayments made—demonstrating how repayments are failing to keep pace with even the cost of borrowing, let alone reducing the principal.-

Advertisements

–

–

By the min 2040’s, the government estimates this to rise to over £500 billion in today’s money. The truth that be simply taking an adjustment of 2,5% inflation, the tru figure will be in excess of £800 billion and I would expect this to be £1 trillion.

–

Government Accounting and Debt Structure

–

Current government accounting methods do not show the full scale of student loan costs within annual expenditure figures. Instead, these liabilities are largely kept off the balance sheet, appearing instead as a growing component of government debt and accruing interest payments.

–

As of now, out of the UK’s £2,800 billion national debt, approximately £266 billion—or nearly 10%—is attributable to student loans. This means the annual interest on student debt alone is close to £10 billion (based on a 10% share of a £105 billion interest bill). Crucially, the total repayments from former students do not cover even this interest, let alone reduce the outstanding capital.

Advertisements

Long-Term Concerns

–

This imbalance raises serious questions about the sustainability of the system. With current interest rates and repayment levels, a significant number of borrowers will never fully repay their loans. Inevitably, a large portion of this debt may have to be written off or absorbed by taxpayers in future—i.e. the very taxpayers who may have taken out student loans themselves.

–

Proposed Solutions

–

Lower Student Loan Interest Rates: Align student loan rates with the Bank of England (BoE) base rate and retroactively recalculate past interest charges. Charging higher rates than the government itself can borrow at is neither fair nor economically rational.

Make Extra Payments Tax-Deductible: Allow any voluntary extra repayments to be deducted from taxable income. This would incentivise early repayment, especially among higher earners, and could, with a 50% take-up rate, add £5–10 billion annually to debt reduction efforts.

Simplify Earnings Thresholds: Introduce a uniform minimum earnings threshold of £25,000 for all borrowers, replacing the current array of thresholds which complicate repayment planning and administration.

–

Assumptions and Next Steps

–

This analysis is based on available public data, with some necessary assumptions regarding the average outstanding loan size and average age of borrowers. These figures will be refined as more information becomes available.

–

Conclusion

–

The current UK student loan system is unsustainable under present conditions. Without reform, the rising tide of student debt will eventually return to the public purse, impacting not just graduates but the entire taxpaying population. The proposed measures offer a starting point for meaningful change, with the aim of building a fairer and more financially robust system for future generations.

Feedback and further suggestions are welcome—this is an issue that demands urgent and informed public debate.

Following the announcement this week, it looks like the Labour government is going to u turn on the Winter Fuel Allowance. My comments are therefore far more limited than they would been.

It is not really a surprise given what a badly implemented policy it was and the way it affected the less well off pensioner. It beggars belief how the government and Rachel Reeves could have thought this was a good idea in the first place.

I suppose the reason was, in their election promises, they said they would not put up income tax and national insurance, but said very little on many other issues. This gave them the opportunity to hit people in their pockets in other ways whilst keeping the facade of not going back on election promises. I wonder how that is working out for them! (no increase in national insurance, smash the gangs!)

But at least now, they are going to backtrack.

The question is to what extent they will roll back this policy? I expect a very limited increase will be announced in the autumn but it will not revert to previous levels of benefit. I also expect it to be complicated to manage causing further waste in Whitehall. We will have to see!

So, if it was up to me, what would i do?

Firstly, I would get on and announce the change, not wait until the autumn. Why wait? If the people in charge can’t come up with a plan and get on with implementation, they should not be in power.

I worked in Civil Engineering for 35 years and knew that deferring a decision was the worst thing we could do. We had to quickly consider the situation and solutions, make a decision and get on with it and live with the consequences.

Secondly, one of the injustices of this allowance , whilst it is to help the vulnerable with their winter fuel bill, it also helps the wealthy pensioners.

So if we were to limit the payments, it would cause a significant amount of administration to means test the benefit. We want to make things simple.

So what i would do, is make it a taxable benefit, so those who pay no tax , get 100% of the benefit. Those on basic taxation they get 80% of the allowance and those on the higher rates will only get 60% of 55% of the allowance.

Doing this means all those getting the state pension would get the allowance included in their OAP payments and HMRC would sort the rest via tax code / tax returns. You do not need extra staff to administer the means testing of individuals.

The above will cost an additional £1.3 billion when compared with 2024/25 (£311m) but save £0.5 billion when compared with 2023/24

And how would I pay for this? Well, as stated in my earlier page on the triple lock, this payment would come out of the massive saving by scrapping the triple lock and just increasing pensions by inflation.

As many people are aware, the UK state pension increases by either, CPI, earnings or 2.5% minimum. This is great for the pensioner, and I will benefit from this when I get to 67. However, I am not sure that people understand how unfair it is on the younger, working age people who are going to get increasing levels of taxation imposed on them to cover the costs.

–

Since the triple lock was introduced (2011), the state pension has increased by 80% whilst inflation has only increase by 55%. Average earnings has increased by 58.8% just keeping ahead of inflation.

–

So, all those below the state retirement age have been paying a higher and higher proportion of their wages / taxes to cover someone else’s state pension.

In fact, if the triple lock continues, the state pension would continue to increase at a higher rate than peoples wages until such time, it becomes impossible to continue due to the size of the black hole in the government’s finances. Things have to change.

–

To understand the scale of the problem, in 2025-26, the UK government is projected to spend approximately £145.6 billion on the state pension which equates to £5100 per household per year.

–

If the increase had been based upon inflation (CPI) alone, the government spending on the state pension would have been about £20 billion less per year.

Over the period of time that the triple lock has been place, I estimate the triple lock has cost the country £120 billion extra (2011 to 2025) than it would have cost, had it been calculated by inflation alone.

–

The problem is only getting bigger.

–

The projected number of those of pensionable age in the UK will increase from the current 13.4 million to 15.6 million in 10 years, which in today’s terms will increase the bill by £26.34 billion (2.2 million x £11,973 per year)

If the level of pension is increase over the next 10 years at the same level of the last 10 years, that will be an increase the cost of the state pension by a further £74 billion resulting in a total annual cost in 2035 of £245 billion.

–

The country cannot afford this level of triple lock increase that, on average, is always going to be more than wages.

–

Don’t get me wrong, I do not want the old and vulnerable to be without food and heat. (Winter fuel allowance to be covered on separate Blog) but many pensioners have other private / company pensions, meaning they are not living on state pension alone.

–

The average personal pension size of someone in their 60’S is £190k which if taking an annuity at 67 would produce and income of over £15k (single life level no guarantee) That is not an insignificant amount, yet they are being increasingly supported by those who are working.

–

It is reported that currently, 70% of pensioners receive income from private pensions. This percentage is increasing due to auto-enrollment in pension schemes which means that, only 7% of those under 35 will relying on state pension alone. This gives ample opportunity and time (42 years) to reduce this percentage.

–

The other problem with the triple lock happened for the 2 years 2023/24 and 2034/25.

–

In 2023/24, the pension was adjusted by 10.1% as it was higher than the wage increase of 5.54%. However, the year later, wage rises rose by 8.5%, basically because wages were increased due to the effects of inflation the previous year. —

So the pension had the effect of the inflation of 2023/24 in both years. None of the political parties wanted to rock the boat as an election was coming up and did not want to address the situation.

–

My solution

Scrap the triple lock and just link State Pension Increases to Inflation. This should keep the status quo for pensioners so that they are no better or worse off due to inflation.

This would save £34 billion per year (in the year 2034/35) if the increase was based upon what happened over the last 10 years with a total saving over 10 years of £190 billion.

I hear in my head all those critics that say, well the last 10 years have been exceptional, due to covid and the effects of the Ukraine war on fuel costs, which I am inclined to agree with.

I estimate that if we exclude the extreme triple lock adjustment years, the saving would still be £18 billion or £79 billion over 10 years. The pensioners will still get increase covering inflation / cost of living so that they are no worse or better off. If they wish to be better off, they need to do that as an individual by having a job or making provision before retirement, as 70% of people already do and 93% of under 35’s do.

Do not allow opt out of Private Pension.

Self employed required to make pension provision and this must be detailed on annual tax return.

The pensions credit system remains as is, allowing a top up to pensions for those who fall short. Overtime as more people retire with some form of Personal Pension, the cost of this will fall.

Use some of this money to reinstate the Winter Fuel Payment to those whose income is below a certain level. Those high earning pensioners do not need it and should be excluded (A separate Blog on this subject will be done in due course) This would cost a max of £1,889 billion of the saving (£2.2 billion(2024 cost) minus 0.311 billion(2025 cost)

–

Conclusion

All the Major parties should get together and agree on the removal of the Triple lock. However, I fear none of them have the bottle and there will always be one who will pledge to keep it on the hope it will get them into power.

However, I think if this is all explained in detail why we cannot continue, the vast majority of the pensioners will understand, after all, those with private pensions have all benefited from the tax breaks that have helped build up their pension pots.

Having retired (early), I have more time on my hands to get annoyed at the news and politicians. (becoming a grumpy old man).

–

I hear comments on the radio from people that just want to criticise with very few coming up with practical solutions that could work.

–

As for the politicians, they just say the opposite of the others and I think their conduct on many occasions is poor and rude. These politicians should be held to the highest of standards but all too often, they fall short.

–

Advertisements

I have been waiting to see what Reform would have to say, given their increase in popularity. My concern is that they are slipping into the same old roll of telling the public what they want to here, without a credible financial plan on how this can be achieved. This week there was talk of increasing the personal tax allowance to £20k. Whilst we would all welcome it, where will the money come from and by when. We cannot complain about public services if we are not prepared to pay our taxes.

–

Labour, with their large majority have made several major blunders including Winter fuel allowance, Employees NI and Inheritance tax on pensions and farms (I am not sure many people appreciate the consequences of this). Yes,they needed to control the spend and try and balance the budget, but I thinks they have gone about it the wrong way. I do not think the public will forgive them.

–

As for the Conservatives, not sure what to say, they are in a state of flux, without identity and clear direction.

–

The LibDems, they should sit in the centre, but they seem too bland.

–

What we need is a party that will sit in the centre and take policies from both sides as it sees fit, but all the parties are too stuck in their ways. I wonder if any of the Parties have the capability to adapt over the coming years to put the “Great” back in Britain.

–

Advertisements

So, my Blog is to take some of the problems issues we have as a country and come up with workable solutions, I intend to explain my logic and as best i can have the financial basis for my proposals.

–

The subjects that annoy me currently are

Winter Fuel Allowance

Increase in Employers National Insurance

Inheritance tax on Pension Pots.

Student loans.

Changes to non-dom status and the exodus of the wealthy

Stamp Duty on Housing

Paying For illegal Immigrants (Not genuine asylum seekers)

Politicians making statement that fall flat when confronted with reality “Smash the Gangs” etc

–

So, I think I will comment on the above over the coming months and put forward my potential solutions that I would implement if it was up to me. (Ifitwasup2me).

–

I would welcome constructive feedback to my comments and would alter my views based upon reasoned arguments.

Hi, I thought, instead of whinging about some of the problems facing the country / world, I would put my thoughts on paper detailing my solutions, if it was up to me.

So hopefully, my future comments may instigate some useful feedback and debate on the issues i raise.

Leave a comment