A Critical Look at Government Claims and the Real Economic Impact

–

Introduction

–

In 2025, the government has asserted that rising pay combined with falling inflation is a win-win for everyone. However, a closer examination reveals a more complicated picture. With average pay rises of 6.6% in the public sector and 4.2% in the private sector, set against an October inflation rate of 3.6%, it is vital to assess whether these increases genuinely benefit workers, and to explore the broader implications for the economy.

–

Pay Rises in 2025: Public vs Private Sector

–

The figures for 2025 paint a tale of two economies. Public sector workers have seen average pay increases of 6.6%, while their private sector counterparts have received an average 4.2% rise. At first glance, both groups may appear to be better off – their nominal pay packets have grown compared to the previous year.

–

However, these headline numbers do not tell the full story.

–

Inflation Context: The October 2025 Rate

–

Inflation, the general rise in prices, stood at 3.6% in October 2025. This means that, on average, the cost of goods and services increased by 3.6% over the previous year. For a pay rise to deliver a real-terms increase in living standards, it needs to outpace inflation. Anything less, and workers may find their extra income is simply absorbed by higher prices.

–

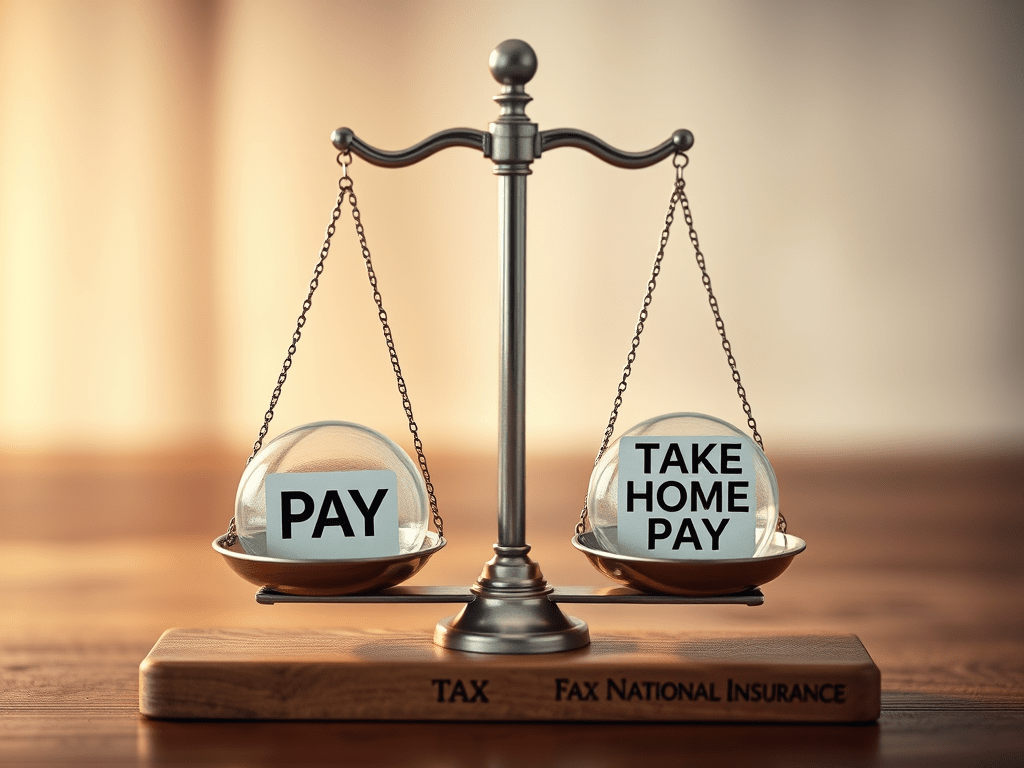

The Impact of Tax, National Insurance, and Pensions

–

Most workers do not receive the full benefit of their pay increases. Standard deductions include income tax (20%), national insurance contributions (8%), and typical pension contributions (5%). Combined, these deductions reduce the headline pay rise by around 33%. In effect, only two-thirds of any pay increase actually reaches workers’ pockets.

–

For example, a £1,000 nominal pay rise leaves just £670 after deductions. This significant reduction means that even a pay rise which appears healthy on paper may not be enough to keep pace with rising costs, especially for those in the private sector where increases are already more modest.

–

Public vs Private Sector: Who Gains, Who Loses?

–

Once deductions and inflation are taken into account, the real-terms situation becomes clear. Private sector workers, with an average 4.2% pay rise, see their increase reduced to roughly 2.8% after deductions. Since this is lower than the 3.6% inflation rate, their real income has actually fallen – their pay does not stretch as far as it did last year.

–

Public sector workers, on the other hand, fare slightly better. Their 6.6% average pay rise, reduced by one third, results in about a 4.4% net increase. After accounting for inflation, public sector workers enjoy a real-terms pay rise of around 0.8%. This is only possible because public sector pay is directly funded by the government, which can make policy decisions to support higher wage settlements.

–

The Employer National Insurance Factor

–

For private sector employers, pay rises are not just a matter of higher wages. They must also pay employer national insurance contributions on increased salaries, adding further costs. This additional expense can lead employers to restrict pay rises, limit hiring, or even reduce jobs. As a result, the private sector faces a double squeeze: rising costs and limited ability to pass on pay increases that match inflation.

–

Economic Consequences: Shrinking Private Sector, Public Sector Pressures

–

The uneven distribution of pay rises has wider economic implications. If private sector pay lags behind inflation, workers’ purchasing power drops, which can suppress consumer spending and slow economic growth. Fewer jobs or lower pay in the private sector also mean less tax revenue and higher welfare costs for the government.

–

Conversely, sustained above-inflation pay rises in the public sector, funded by the government, raise questions about long-term sustainability. With public finances already under pressure, continued high wage settlements and generous pension commitments could strain budgets, potentially leading to higher taxes or cuts in services elsewhere.

–

Summary and Conclusion

–

The government’s claim that rising pay and falling inflation benefit everyone does not bear out under scrutiny. In 2025, private sector workers are losing out in real terms, as their take-home pay increases lag behind inflation after deductions. Public sector workers are better protected, but only because government funding has enabled pay rises that outpace inflation – a situation that may not be sustainable in the long run. We cannot keep increasing taxes on the private sector to cover the public sector. You will end up with no workers.

–

The knock-on effects include increased pressure on private sector employers and potential job losses, alongside growing fiscal challenges for the public sector. In reality, the benefits of rising pay and falling inflation are unevenly distributed, and both employees and policymakers must recognise the complexity behind the headline figures if they are to make informed decisions about the country’s economic future.

Leave a comment